Yes, It’s Coming Soon…

With Apple (AAPL) confirming the date of its next event (September 9) the rhetoric about the iPhone 17 line continues to grow. We see, on a daily basis, “The 5 Improvements Apple will make for the iPhone 17..” or similar headlines with the same leaked or speculated changes that have been detailed hundreds of times over. Some of these change reports are supported by ‘industry professionals’, or ‘those with knowledge of the matter”, or even ‘conversations with suppliers’, although we expect that Apple has control over most of these sources and uses them strategically to generate excitement leading up to the event.

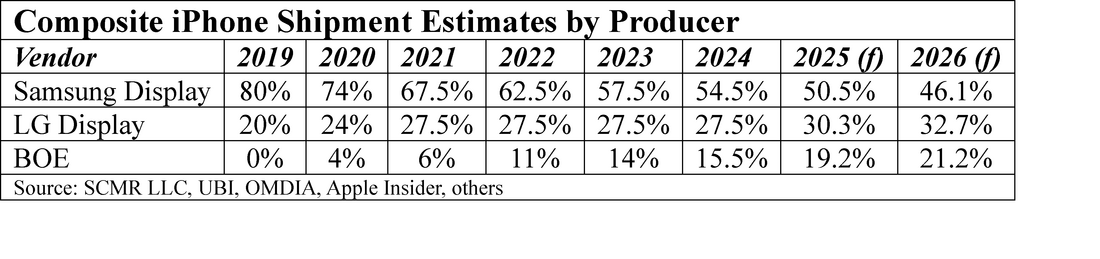

Rather than dwell on these changes, most of which seem rather mundane, we look more toward the effect the iPhone 17 series will have on the smartphone ecosystem. The Korean research firm UBI has been kind enough to share its thought on the production of displays for Apple smartphones this year and next, which we highlight, rather than dwell on whether the iPhone 17 will come in 3 colors or 4. As we have previously noted, iPhone displays ae typically produced by three suppliers, Samsung Display (pvt), LG Display (LPL) and BOE (200725.CH). There have been other in the past (Sharp (6753.JP), Japan Display (6740.JP), etc.) but when it comes to OLED displays, the three named above are the key suppliers. Unfortunately not all sources agree on the percentages for each, but we have pulled together an amalgam of data that is a composite of the industry estimates for the past six years along with UBI’s projections for this year and next. We note that due to averaging not all years equal 100%..

Rather than dwell on these changes, most of which seem rather mundane, we look more toward the effect the iPhone 17 series will have on the smartphone ecosystem. The Korean research firm UBI has been kind enough to share its thought on the production of displays for Apple smartphones this year and next, which we highlight, rather than dwell on whether the iPhone 17 will come in 3 colors or 4. As we have previously noted, iPhone displays ae typically produced by three suppliers, Samsung Display (pvt), LG Display (LPL) and BOE (200725.CH). There have been other in the past (Sharp (6753.JP), Japan Display (6740.JP), etc.) but when it comes to OLED displays, the three named above are the key suppliers. Unfortunately not all sources agree on the percentages for each, but we have pulled together an amalgam of data that is a composite of the industry estimates for the past six years along with UBI’s projections for this year and next. We note that due to averaging not all years equal 100%..

While Samsung Display’s share has been declining, we note that the sales value of each iPhone model are different and in most years SDC was the dominant or sole display supplier of the higher value models while BOE tends to provide the more generic lower value models, skewing the sales value in SDC’s favor each year. In most years SDC maintains its current year share, while ceding some earlier year production to others. BOE has had a difficult time competing with its South Korean rivals as it has had qualification issues that have limited its production in the past, particularly on high-end models. In 2022 it was found that BOE made a change in the design of the iPhone 13 it was producing without Apple’s authorization, for which it was punished with reduced shipment targets that year. But Apple needs BOE to keep display costs down and rein in Samsung’s premium pricing, and based on UBI’s forecasts, despite the issues, BOE seem to be making progress toward establishing a firmer relationship with Apple, barring an legal issues[1].

One additional point. Samsung recently won the exclusive contract to supply both the display and the hinge to Apple’s foldable phone in 2026, although LGD and BOE are expected to supply the non-foldable display on the device, although the proportions have yet to be decided. We expect this will improve SDC’s production share with Apple despite the relatively small number of units to be produced, as the foldable display will carry a significant premium.

[1] Samsung recently won an ITC ruling that could make it more difficult for BOE to supply certain displays in the US.

One additional point. Samsung recently won the exclusive contract to supply both the display and the hinge to Apple’s foldable phone in 2026, although LGD and BOE are expected to supply the non-foldable display on the device, although the proportions have yet to be decided. We expect this will improve SDC’s production share with Apple despite the relatively small number of units to be produced, as the foldable display will carry a significant premium.

[1] Samsung recently won an ITC ruling that could make it more difficult for BOE to supply certain displays in the US.

RSS Feed

RSS Feed